Connecticut_Courtroom_Real_Property_Settlement

CT LAW State Portion Exam: Your Complete PSI CT Law Portion Exam Study Guide

By Capital Real Estate School | Real Estate Licensing Exam Prep Series

Real Estate Brokerage and Agency: CT Law Portion Exam Review.

What does a Connecticut real estate broker or salesperson legally need to do before representing a client?

In Connecticut, a real estate license is required for anyone who, for another person and for compensation, negotiates, sells, leases, or offers to buy or exchange real estate. Unlicensed activities include administrative tasks like answering phones or making appointments, but negotiating any terms of a deal always requires a license.

Connecticut operates under a fiduciary duty framework. A licensee representing a client must provide the following:

- COALD — Care, Obedience, Accounting, Loyalty, and Disclosure

Types of agency relationships in CT:

| Relationship | Who Is Represented |

| Seller’s Agent | Seller only |

| Buyer’s Agent | Buyer only |

| Dual Agent | Both parties (with written consent) |

| Designated Agency | Each party has its own agent within the same firm |

| Facilitator | Neither party has a fiduciary duty |

PSI Exam Tip: Expect 2–3 questions on the difference between a facilitator and an agent. In CT, a facilitator owes no fiduciary duty but must still treat both parties honestly and fairly. Dual agency in CT requires informed written consent from all parties.

Record Retention: Connecticut licensees must retain transaction records for 7 years.

Client Representation Agreements

What must a Connecticut listing agreement include by law?

Written agency agreements are required in CT before a broker or licensee may negotiate a sale, purchase, exchange, or lease. The written agreement must include:

- Property identification

- Compensation terms

- Start and expiration dates

- Type of agency relationship

- Signatures and addresses of all parties

Types of listing agreements:

| Type | Key Feature |

| Exclusive Right to Sell | The broker earns commission regardless of who sells |

| Exclusive Agency | The owner may sell without owing a commission |

| Open Listing | Multiple brokers; only the selling broker earns |

| Net Listing | Broker keeps all above a set net price (rare; risky) |

PSI Exam Tip: The Exclusive Right to Sell is the most tested listing type. Know that CT law requires agency agreements to state that broker compensation is NOT fixed by law and is negotiable. This statement must be in at least 10-point boldface type.

A Prospective Parties Disclosure Notice must be provided to any prospective client at the first personal meeting.

Interests in Real Estate

Connecticut recognizes different types of interests a person can hold in real estate, from full ownership (fee simple) to partial rights, such as easements.

Key types of real estate interests:

- Fee Simple Absolute: Complete ownership with no conditions

- Life Estate: Ownership limited to a person’s lifetime

- Easements: The right to use another’s land for a specific purpose

- Easement by Prescription: Acquired through open, continuous, hostile use (like adverse possession but for use, not ownership)

- Water Rights: CT recognizes riparian rights (rights of landowners along waterways)

PSI Exam Tip: Know the difference between an easement appurtenant (attached to the land and transfers with the deed) and an easement in gross (a personal right that does not transfer). CT exam questions often ask which type survives a property sale.

Forms of Real Estate Ownership

What is the difference between joint tenancy and tenancy in common in Connecticut?

| Feature | Joint Tenancy | Tenancy in Common |

| Right of Survivorship | YES, survivor inherits | NO, it passes to heirs |

| Equal Shares Required | YES | NO, unequal shares allowed |

| Number of Owners | 2 or more | 2 or more |

| Common in CT | Less common | Most common form |

Connecticut Common Interest Ownership Act (CIOA): Governs condominiums, cooperatives, and planned communities. All new common interest communities must comply with CIOA. This unit also addresses time-share interests.

PSI Exam Tip: Know that Connecticut’s CIOA requires a public offering statement for the sale of new condominium units. Furthermore, memorize the four unities required for joint tenancy: Time, Title, Interest, and Possession (TTIP).

Legal Descriptions

Three methods are used to legally describe real estate in Connecticut:

- Metes and Bounds: The oldest method, using distances and directions from a point of beginning (POB). This method is most common in New England, including CT.

- Lot and Block (Plat Map): Used in subdivisions; it refers to a recorded plat.

- Monument Method: Uses physical landmarks (less precise; rarely used alone).

PSI Exam Tip: For CT, know that metes and bounds is the dominant method. A legal description must always be able to return to its point of beginning to be valid. Common interest community units are described under the CIOA using a unit-designation and common-element approach.

Real Estate Taxes and Other Liens

How are property taxes calculated in Connecticut?

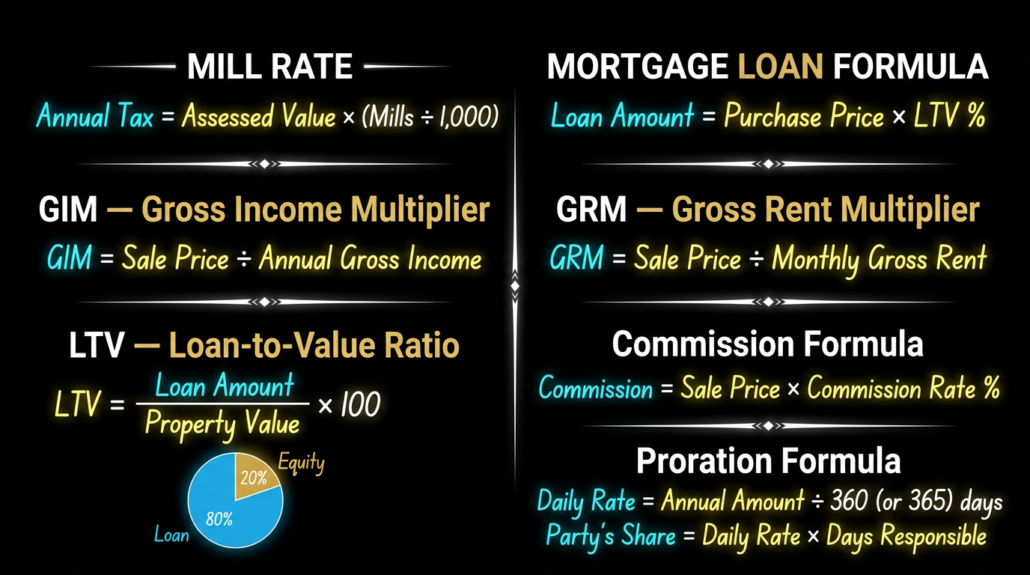

Connecticut assesses property at 70% of fair market value. The tax rate (mill rate) is expressed as dollars per $1,000 of assessed value.

Formula: Assessed Value × Mill Rate ÷ 1,000 = Annual Tax

Priority of Liens in CT (General Order):

| Priority | Lien Type |

| 1st | Real estate tax lien |

| 2nd | Special assessment liens |

| 3rd | Mechanic’s liens |

| 4th | Mortgage liens (by recording date) |

| 5th | Judgment liens |

Other key CT taxes:

- Conveyance Tax (Transfer Tax): CT charges a conveyance tax on deed transfers. The rate is tiered based on sale price and property type.

- Use Tax / Mil Rate: Set by local municipalities; varies by town.

PSI Exam Tip: CT exam questions often focus on property tax assessment at 70% and calculating taxes using the mill rate. Also know that real estate tax liens take priority over mortgage liens regardless of recording date. There are no actual math questions on this portion of the PSI Exam.

Real Estate Contracts

What are the essential elements of a valid real estate contract in Connecticut?

For any contract to be legally enforceable:

- Offer and Acceptance (mutual assent)

- Consideration (something of value exchanged)

- Legally competent parties

- Legal purpose

- Statute of Frauds: Real estate contracts must be in writing to be enforceable in CT

Key contract types in CT:

| Contract Type | Purpose |

| Purchase and Sale Agreement | Primary residential sales contract |

| Option Contract | The buyer pays for the right to purchase later |

| Land Contract (Installment Sale) | The seller retains title until paid in full |

| Lease with Option to Buy | Combines a lease with a purchase option |

Residential Property Condition Report: Sellers of residential property (1–4 units) must provide buyers with a written Property Condition Disclosure Report (CGS §20-327b). Failure to provide it requires a $500 credit to the buyer at closing.

PSI Exam Tip: Know the $500 credit rule for failing to deliver the Property Condition Report. Furthermore, memorize that real estate contracts must be in writing (Statute of Frauds) and that an acceptance must mirror the offer exactly; any change creates a counteroffer, not an acceptance.

Transfer of Title

What type of deed provides the greatest protection to a buyer in Connecticut?

| Deed Type | Warranty Level |

| General Warranty Deed | Full warranty against all claims — best protection |

| Special Warranty Deed | Warranty only against the grantor’s own acts |

| Quitclaim Deed | No warranty, transfers only what the grantor owns |

| Bargain and Sale Deed | No express warranties are implied; ownership |

Real Estate Conveyance Tax: CT imposes a tax on property transfers. The base rate is 0.75% on the first $800,000 and 1.25% on amounts above $800,000 for most residential properties. There is also a municipal conveyance tax of up to 0.25%. Please Note: There are no actual math questions on this portion of the PSI Exam.

Adverse Possession in CT: A person may gain title to property through open, notorious, continuous, hostile, and actual possession for 15 years (prescriptive period) in Connecticut.

PSI Exam Tip: Know all deed types and their warranty levels. Furthermore, memorize the 15-year period for adverse possession in CT (not 10 or 20, a common trick question). The CT conveyance tax rates are frequently tested.

Title Records

Why is recording a deed important in Connecticut?

Recording provides constructive notice to the world that ownership has changed. Connecticut uses a race-notice recording system; the first person to record without notice of prior claims wins.

Evidence of Title Methods:

| Method | Description |

| Abstract of Title | Summary of all recorded documents |

| Attorney’s Title Opinion | Lawyer’s review of abstract |

| Title Insurance | Policy protecting against defects (owner’s or lender’s) |

| Torrens System | Court-certified title registration (rare in CT) |

Marketable Record Title Act (MRTA): CT has adopted this act, which limits title searches to a 40-year period. Claims older than 40 years are generally extinguished unless a notice is filed to preserve them.

PSI Exam Tip: The 40-year MRTA search period is a high-frequency CT exam topic. Also, know the difference between an owner’s title insurance policy (one-time premium, protects the buyer) and a lender’s title insurance policy (protects only the mortgage lender).

Real Estate License Law (Highest Exam Priority)

What are the Connecticut real estate license requirements, fees, and renewal rules?

CT Real Estate Commission

The Connecticut Real Estate Commission (under the Department of Consumer Protection) oversees all licensees. It has the authority to grant, suspend, revoke, and reinstate licenses.

License Types and Requirements

| License Type | Education Required | Experience | Exam |

| Salesperson | 60-hour pre-license course | None | PSI exam (national + state) |

| Broker | 60-hour pre-license course | 2 years as active salesperson | PSI exam |

| Appraisal Licenses | Varies by category | Varies | Separate exam |

License Renewal and Continuing Education

| Requirement | Details |

| Renewal Period | Every 2 years |

| CE Hours Required | 12 hours per renewal period |

| Required CE Topic | Fair Housing (mandatory every renewal) |

| Inactive Status | License kept without practicing |

Conduct of Licensees: Key Rules

- Trust Accounts: All client funds must be deposited in a separate escrow/trust account within 3 banking days of the signed agreement.

- Advertising: No blind ads allowed. All ads must display the licensee’s name, the supervising broker’s name, and the supervising broker’s contact information.

- Disclosure of Interest: Licensees must disclose in writing any personal interest in a property being bought or sold (CGS §20-328-2a).

- Compensation: Cannot be shared with unlicensed individuals. Must be paid through the broker, not directly from a client to the salesperson.

- Custodial Broker: Appointed when a broker dies or becomes incapacitated; may serve for up to 180 days.

- Referral Fees: Cannot be paid to unlicensed individuals engaging in the CT real estate business.

Grounds for License Suspension or Revocation

| Violation | Potential Penalty |

| Misrepresentation or fraud | Revocation |

| Commingling client funds | Fine up to $1,000 and/or 6 months imprisonment |

| Violations of fair housing law | Suspension/revocation |

| Failure to disclose the agency | Suspension |

| Unlicensed practice | Criminal penalties |

Real Estate Financing: Principles/Practice

What is the difference between a mortgage deed and a promissory note in Connecticut?

In CT, a mortgage transaction involves two documents:

- Promissory Note: The borrower’s promise to repay the debt

- Mortgage Deed: The document pledging the property as collateral

CT is a modified title theory state: the lender technically holds title during the loan period, though the borrower retains possession, and a formal foreclosure process.

Foreclosure in CT: Connecticut uses judicial foreclosure (court process). Two types:

- Strict Foreclosure: The court sets a deadline; if the borrower doesn’t pay, title passes directly to the lender.

- Foreclosure by Sale: Property is sold; borrower may receive surplus proceeds

Predatory Lending: CT has strict protections against predatory lending practices, particularly for high-cost home loans.

PSI Exam Tip: CT is one of only a few title theory states still using strict foreclosure; both facts appear regularly on the PSI exam. Know the difference between a mortgage deed (security instrument) and a promissory note (debt obligation).

Leases

What are a landlord’s and tenant’s rights and obligations under Connecticut’s Landlord and Tenant Act?

Connecticut’s Landlord and Tenant Act (CGS §47a) is heavily tested on the PSI exam. Key provisions:

Security Deposits

| Tenant Age | Maximum Security Deposit |

| Under 62 years old | 2 months’ rent |

| 62 years old or older | 1 month’s rent |

| Return deadline | 30 days after move-out (15 days if no deductions) |

Landlord Obligations

- Maintain premises in a fit and habitable condition

- Comply with applicable building and housing codes

- Provide heat from October 1 to May 1 (residential)

- Make all repairs not caused by the tenant

Tenant Obligations

- Pay rent on time

- Keep the unit clean and undamaged

- Do not disturb other tenants

- Allow reasonable landlord entry (with proper notice)

Eviction (Summary Process)

CT’s summary process (eviction) requires the following:

- Written notice to quit (typically 3 days for nonpayment)

- Court filing if the tenant does not vacate

- Judge’s decision: if the tenant loses, the marshal enforces

Real Estate Appraisal

What are the four CT appraisal license categories?

| License/Certification | Scope of Practice |

| Trainee | Works under the supervision of an appraiser |

| Licensed Residential | Non-complex 1–4 unit residential |

| Certified Residential | All residential property |

| Certified General | All property types, including commercial |

The three approaches to value tested on PSI are:

- Sales Comparison Approach: Most common for residential property

- Cost Approach: Best for new construction and special-use property

- Income Approach: Used for income-producing property

PSI Exam Tip: Know that the Sales Comparison Approach is typically preferred for single-family homes. The Income Approach uses the capitalization rate (Cap Rate = NOI ÷ Value). CT appraisers are regulated under the Real Estate Appraisal Commission. Please note: There are no actual math questions on this portion of the PSI Exam.

Land-Use Controls and Property Development

What is the purpose of zoning in Connecticut?

Zoning divides land into districts controlling the use, height, and density of buildings. Connecticut’s zoning is administered by local municipalities, not the state.

Key Land-Use Tools:

| Tool | Purpose |

| Zoning Ordinance | Regulates permitted uses by district |

| Variance | Permission to deviate from zoning rules |

| Special Exception (Use Permit) | Permitted use requiring additional approval |

| Nonconforming Use | Pre-existing use that doesn’t comply with current zoning |

| Subdivision Regulations | Control how land is divided |

Connecticut Interstate Land Sales: Large subdivisions (25+ lots) offered across state lines may require registration under the Interstate Land Sales Full Disclosure Act (ILSFDA). CT also has its own regulations for large-scale developments.

PSI Exam Tip: Distinguish between a variance (hardship-based deviation) and a special exception (conditionally permitted use). Know that nonconforming uses are allowed to continue, but generally cannot be expanded. Eminent domain (the government’s power to take private property for public use) requires just compensation.

Fair Housing (Highest Exam Priority)

What classes are protected under both federal and Connecticut fair housing laws?

Federal Fair Housing Act (1968) — Protected Classes

Race, Color, Religion, Sex, National Origin, Familial Status, Disability (Handicap)

Connecticut Additional Protected Classes

Connecticut adds several classes beyond federal law:

| CT-Only Protected Class | Notes |

| Age | Any age (not just familial status/children) |

| Marital Status | Single, married, divorced |

| Sexual Orientation | Including gender identity and expression |

| Lawful Source of Income | Section 8 vouchers, child support, etc. |

| Veteran Status | Veterans and active military |

| Victims of Domestic Violence | Protected in housing decisions |

| “Clean Slate” (Erased Criminal Records) | May not use expunged records in housing decisions |

| Physical, Mental, or Learning Disability | Broader than the federal definition |

| Ethnic Origin | Specifically listed |

Discriminatory Practices: Prohibited Actions

- Steering: Directing buyers/renters toward or away from neighborhoods based on protected class

- Blockbusting: Inducing owners to sell by suggesting protected groups are moving in

- Redlining: Denying loans/insurance based on neighborhood demographics

- Discriminatory Advertising: Any preference or limitation based on a protected class

Closing the Real Estate Transaction

What happens at a Connecticut real estate closing?

In CT, closings are typically handled by an attorney. Key closing documents and concepts:

| Document | Purpose |

| Closing Disclosure (CD) | Final summary of loan costs (required 3 business days before closing) |

| HUD-1 Statement | Used for non-RESPA transactions |

| Deed | Transfers legal title from seller to buyer |

| Promissory Note | Buyer’s promise to repay the mortgage |

| Mortgage Deed | Secures the lender’s interest in the property |

Prorations at Closing: Property taxes, rents, and HOA fees are prorated between buyer and seller based on the closing date. CT uses a 365-day year for proration calculations (actual/actual method).

PSI Exam Tip: Buyers receive the Closing Disclosure at least 3 business days before closing (a TRID/RESPA requirement). Practice proration math using the 365-day method. Understand the seller’s net sheet and buyer’s estimated closing costs.

Environmental Issues and the Real Estate Transaction

What environmental hazards must Connecticut real estate licensees know about?

| Hazard | Key Facts for CT Exam |

| Lead-Based Paint | Disclosure required for pre-1978 homes; federal law |

| Asbestos | Common in pre-1980 insulation and tiles |

| Radon | Odorless gas; CT has elevated radon levels; testing recommended |

| Underground Storage Tanks (USTs) | Liability risk; must be removed or properly closed |

| Wetlands | CT DEP regulates wetland disturbances |

| Hazardous Waste (Superfund) | Sellers must provide notice of CTDEEP list availability |

| Urea-Formaldehyde Foam Insulation | Banned from use; disclosure required if present |

Off-Site Conditions: CT law excuses seller/agent liability for off-site hazardous waste if written notice is provided to buyers about the CTDEEP list at or before signing the purchase contract (CGS §20-327f).

PSI Exam Tip: The off-site hazardous waste written notice rule is CT-specific and frequently tested. Also know that lead-based paint disclosure is a federal requirement for all homes built before 1978 and that buyers have a 10-day window to conduct lead testing (they can waive this right).

Real Estate Securities

When does selling real estate become regulated as a securities transaction in Connecticut?

Real estate becomes a security when buyers invest primarily for profit from others’ efforts, rather than for personal use. This rule applies to:

- Real Estate Investment Trusts (REITs)

- Real estate syndications and limited partnerships

- Fractional interests sold as investments

CT Regulations: Connecticut follows the Uniform Securities Act for real estate securities. Any offer or sale of real estate securities in CT must be registered or exempt. The CT Department of Banking regulates securities offerings.

PSI Exam Tip: The key test for whether real estate is a security: Is the buyer relying on the efforts of others to generate profit? If so, it is a security. Know that REITs allow investors to pool money to invest in large real estate portfolios. Unlicensed individuals selling real estate securities face serious legal consequences.

Top 10 PSI CT Law Exam Tips

What are the most important things to know for the PSI Connecticut Law exam?

| # | Tip | Unit |

| 1 | Trust account deposit = 3 banking days from signed agreement | 10 |

| 2 | Property assessed at 70% of fair market value in CT | 6 |

| 3 | Adverse possession = 15 years in CT | 8 |

| 4 | Security deposit max = 2 months (1 month if tenant is 62+) | 12 |

| 5 | CT Marketable Record Title Act = 40-year search limit | 9 |

| 6 | CT adds 8+ protected classes beyond federal fair housing | 15 |

| 7 | CT is a title theory / strict foreclosure state | 11 |

| 8 | Property Condition Report failure = $500 buyer credit | 7 |

| 9 | Compensation is NOT fixed by law, must say so in 10-point bold | 2 |

| 10 | A custodial broker may serve up to 180 days | 10 |

Quick-Reference: Key CT Statutes and Numbers

| Topic | CT Statute / Rule |

| License Law | CGS §20-311 et seq. |

| Agency Disclosure | CGS §20-325d |

| Property Condition Disclosure | CGS §20-327b |

| Landlord and Tenant Act | CGS §47a |

| Fair Housing (CT) | CGS Title 46a, Chapter 814c |

| Environmental Disclosure | CGS §20-327f |

| Record Retention | 3 years |

| Trust Account Deposit | Within 3 banking days |

| License Renewal | Every 2 years |

| CE Hours Required | 12 hours / 2 years |

| Adverse Possession | 15 years |

| Property Assessment Rate | 70% of fair market value |

| MRTA Search Period | 40 years |

| Security Deposit Max (under 62) | 2 months’ rent |

| Security Deposit Max (62+) | 1 month’s rent |

| Security Deposit Return | 30 days (15 days if no deductions) |

| Custodial Broker Duration | Up to 180 days |

Exam Strategy: How to Approach PSI CT Law Questions

- Read the question twice. PSI questions often include “except,” “most likely,” or “which of the following is NOT”; these reverse the expected answer.

- Look for CT-specific clues. If a question involves a number (days, percentages, months), it is almost always testing a CT-specific rule. Use the tables above.

- Eliminate first. Cross out answers that are clearly wrong before choosing. Two answers are usually close; pick the one that is more specific to Connecticut law.

- Agency = written agreement. For any question about when agency begins in CT, remember: no written agreement = no agency relationship recognized by the Commission.

- Fair housing = broadest protection wins. When in doubt, CT law is more protective than federal law. In Connecticut, if federal law does not include a CT class, the CT rule applies.

This article is intended only as an educational study guide for the PSI State Portion exam preparation and does not constitute legal advice.

Good luck on your PSI exam! Remember, understanding valuation isn’t just about passing the test. It’s one of the most practical skills you’ll use every single day in your real estate career.

Tags: Connecticut real estate law, PSI exam prep, CT real estate license, real estate exam tips, CT law exam, license law Connecticut, agency relationships, fair housing Connecticut, landlord-tenant CT, security deposit CT, real estate contracts, property disclosure CT, CT deed types, adverse possession, conveyance tax CT, property tax CT, mill rate, title search CT, real estate appraisal, CT zoning law, CIOA Connecticut,

(c) Capital Real Estate School, LLC

(c) Capital Real Estate School, LLC

(c) Capital Real Estate School, LLC

(c) Capital Real Estate School, LLC

(c) Capital Real Estate School, LLC

(c) Capital Real Estate School, LLC

@ Capital Real Estate School, LLC

@ Capital Real Estate School, LLC

CRES - Capital Real Estate School, LLC

CRES - Capital Real Estate School, LLC